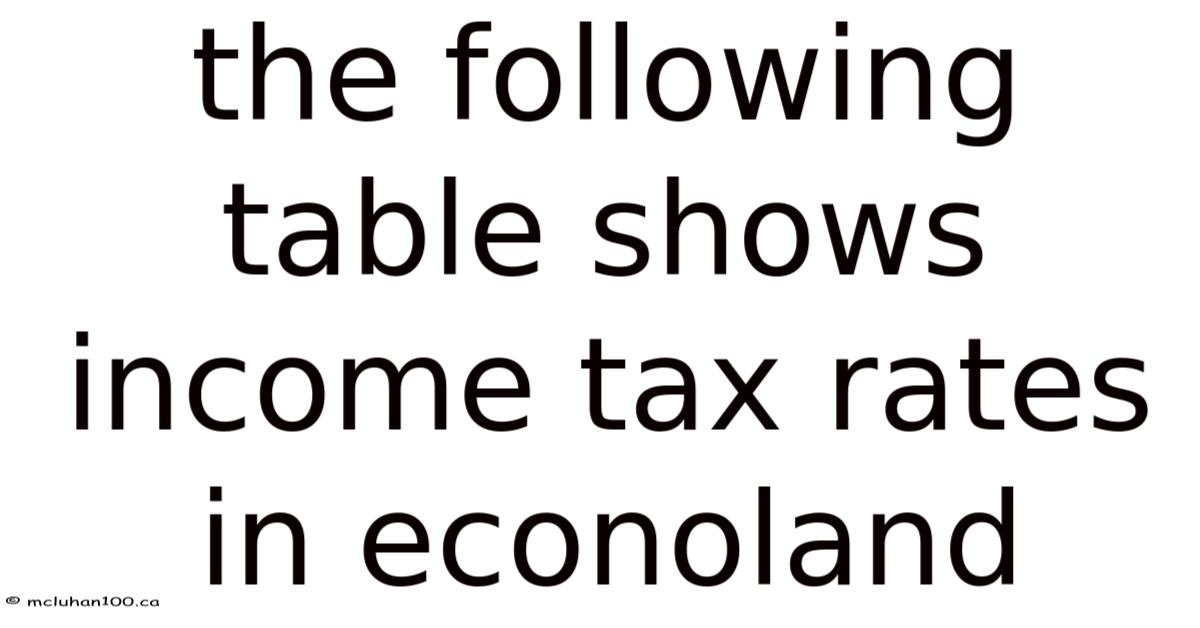

the following table shows income tax rates in econoland

| Income Bracket | Tax Rate |

|---|---|

| 0 - 10,000 | 0% |

| 10,001 - 30,000 | 10% |

| 30,001 - 60,000 | 20% |

| 60,001 - 100,000 | 30% |

| Above 100,000 | 45% |

What Is Income Tax in Econoland

Income tax is the slice taken from what you earn, whether it’s a salary, freelance gig, or a modest side hustle. In Econoland the system is designed to be straightforward: the more you bring in, the higher the percentage you hand over. It’s not a complicated formula, but the brackets can feel a bit odd at first glance. The key is to see it as a sliding scale rather than a series of hard stops.

The Basics

Econoland uses five brackets. If you make under ten thousand, you pay nothing. That's why that’s the idea behind a “zero‑tax” threshold – it lets people keep enough to cover basic needs. In real terms, once you cross that line, the rate climbs gradually. The highest bracket starts at one hundred thousand and sits at forty‑five percent.

Why It Matters

You might wonder why anyone should care about a table of numbers. The answer is simple: tax rates affect everything from where you live to how much you can save Simple, but easy to overlook..

- Budgeting – Knowing your tax rate helps you plan for rent, groceries, and that weekend getaway.

- Career choices – A higher bracket means more take‑home pay disappears, which can influence whether you chase a higher‑paying job or stay in a lower‑stress role.

- Government funding – Taxes feed public services. Understanding the structure shows how the state balances revenue with citizen welfare.

When people ignore the numbers, they often end up overpaying or, worse, under‑planning. Real talk: many folks just glance at the table, assume they’re in the 20% bracket, and forget about the extra 5% that kicks in once they hit the next threshold.

It sounds simple, but the gap is usually here.

How It Works

Understanding Your Bracket

The table isn’t a single rate for the whole year. On top of that, it’s marginal – you pay the rate only on the portion of income that falls inside each bracket. Think of it like climbing a ladder: each rung has its own price tag.

Here's one way to look at it: if you earn 55,000, the first 10,000 is tax‑free. Still, the next 20,000 (from 10,001 to 30,000) is taxed at 10%. That said, the remaining 25,000 (from 30,001 to 55,000) falls into the 20% bracket. You calculate each slice separately and add them up The details matter here..

You'll probably want to bookmark this section That's the part that actually makes a difference..

Filing and Payments

Econoland requires annual filing. You submit a form that lists your total income, then the system automatically applies the marginal rates. Most people pay through withholding from their paychecks, but self‑employed folks need to make quarterly estimates.

Deductions and Credits

There are a few common deductions that lower the effective rate:

- Personal allowance – a set amount subtracted before the brackets kick in.

- Education credits – for each qualifying course, a fixed credit reduces the tax owed.

- Retirement contributions – money put into a pension plan can lower taxable income.

These tools can shift you into a lower bracket without changing your actual earnings.

Common Mistakes

Assuming a Flat Rate

One of the biggest slip‑ups is treating the table as a flat rate. If you earn 80,000, you can’t just multiply by 30% and call it a day. The marginal nature means you’ll actually pay less than a flat 30% because the lower portions are taxed less Nothing fancy..

This changes depending on context. Keep that in mind.

Overlooking Deductions

Many taxpayers skip the personal allowance or forget about education credits. The result? They pay more than necessary.

Ignoring the 45% Bracket

The top bracket feels intimidating, so some high earners try to avoid it altogether. Here's the thing — they might move money into offshore accounts or shift income timing, but those tactics can backfire with penalties. The safest route is to plan ahead and use legal deductions.

Practical Tips

- Run the numbers early – Use a simple spreadsheet to see where you land. Even a rough estimate beats guessing.

- Maximize deductions – Contribute to a retirement plan before the year ends. It lowers taxable income and builds your future safety net.

- Check for credits – If you’re paying for school or childcare, see if a credit applies. It’s often a dollar‑for‑dollar reduction, which is more valuable than a deduction.

- Review each year – Income changes, brackets shift, and new credits appear. A yearly check keeps you from surprise tax bills.

FAQ

What happens if I earn just above a bracket threshold?

You’ll pay the higher rate only on the amount that exceeds the lower threshold. The rest stays taxed at the lower rate.

Can I combine income from multiple sources to stay in a lower bracket?

Yes, but you still need to report the total. The tax system looks at overall income, not the source.

Do I need to file if my income is below 10,000?

If you earn under the zero‑tax threshold and have no other taxable income, you typically don’t need to file. Even so, if you had significant withholding or qualify for a credit, filing can be beneficial Simple as that..

How often are the brackets updated?

Econoland reviews the brackets every two years to account for inflation and policy changes.

Is there a way to reduce the 45% rate?

Legal avenues include maximizing retirement contributions, taking available credits, and structuring income to stay within lower brackets where possible.

Closing Thoughts

Understanding the income tax rates in Econoland isn’t about memorizing numbers; it’s about seeing how those numbers shape everyday decisions. The table provides a clear map, but the real value comes from using that map to plan, save, and make smarter financial moves.

Take a moment to look at your own earnings, run a quick calculation, and see where you sit. Adjust where you can, claim the deductions you qualify for, and keep an eye on the next filing season. In the end, the tax system is just another tool – one that, when used wisely, can help you keep more of what you earn and build a more secure future Small thing, real impact. Turns out it matters..

Since you have already provided the full text of the article, including the conclusion, I will provide a supplementary "Next Steps" section that could follow your text to add even more value, or if you intended for me to write a new section before the "Closing Thoughts," here is a bridge that fits the tone:

The Importance of Professional Guidance

While DIY spreadsheets and basic checklists are excellent for general awareness, there comes a point where the complexity of your finances may outpace simple tools. If your income is approaching the higher tiers or if you have complex assets like rental properties, stocks, or foreign holdings, consulting a tax professional is a strategic investment rather than an expense.

A certified accountant can help you work through the nuances of tax law that a general guide might miss. They can assist with:

- Advanced Tax Loss Harvesting: Offsetting capital gains with losses to lower your overall taxable footprint.

- Estate Planning: Ensuring that your wealth is passed down efficiently without triggering unnecessary tax burdens.

- Audit Protection: Providing the documentation and expertise needed to defend your filings if the authorities request a review.

By combining your own proactive planning with professional expertise, you move from a defensive posture—simply trying to avoid penalties—to an offensive one, where you are actively optimizing your wealth.

Summary of the Article's Flow

If you were looking for a continuation because you felt the "Closing Thoughts" were too abrupt, the section above provides a logical transition from "Practical Tips" to the "Closing Thoughts" by addressing the transition from individual effort to professional management.

Next Steps: Turning Knowledge into Action

Armed with a solid understanding of Econoland’s tax brackets, you’re now positioned to move from theory to practice. The most effective way to capitalize on this knowledge is to treat tax planning as an ongoing, dynamic process rather than a once‑yearly chore. Below are concrete steps you can integrate into your financial routine:

1. Build a Personal Tax Dashboard

Create a simple spreadsheet or use budgeting software that tracks your income sources, deductible expenses, and estimated tax liability month‑by‑month. By visualizing your progress against each bracket threshold, you can anticipate when you might cross into a higher rate and adjust accordingly—perhaps by accelerating deductible contributions or timing capital gains Simple, but easy to overlook..

2. Optimize Deductions and Credits Strategically

- Timing of Income: If you expect a bonus or a large one‑time payment, consider deferring receipt to the next tax year if it would push you into a higher bracket.

- Accelerating Expenses: Prepaying deductible items such as mortgage interest, charitable contributions, or retirement plan contributions can lower your taxable income for the current year.

- Credit Utilization: Review eligibility for education, energy‑efficiency, or healthcare credits. Even modest credits can shave thousands off your tax bill.

3. make use of Tax‑Advantaged Accounts

Maximize contributions to retirement accounts (RRSPs, 401(k) equivalents) and health savings accounts (HSAs). These vehicles not only reduce taxable income but also provide long‑term growth or savings benefits that compound over time.

4. Conduct a Mid‑Year Review

A quick check in July or August can reveal whether your current trajectory aligns with your tax goals. If you’re on track to exceed a bracket threshold, you might adjust withholding or make additional deductible payments before year‑end.

5. Engage a Professional When Complexity Grows

While the fundamentals can be managed independently, certain scenarios benefit from expert oversight:

- Multiple income streams (e.g., freelance work, rental income, investments) that blur the lines between ordinary and capital gains.

- Cross‑border elements such as foreign earnings or holdings.

- Significant asset transfers like inheritances, large gifts, or business ownership changes.

A qualified accountant or tax advisor can uncover opportunities—such as tax‑loss harvesting or strategic estate planning—that go beyond the scope of a standard guide.

6. Stay Informed About Legislative Changes

Tax laws can shift from year to year. Subscribing to reputable tax newsletters, following your local revenue agency’s updates, or setting calendar alerts for filing deadlines ensures you never miss a critical adjustment that could affect your bracket.

Conclusion

Understanding Econoland’s income tax brackets is the foundation of smart financial management. By mapping your earnings against these brackets, strategically timing deductions and credits, and maintaining a proactive tax dashboard, you transform a potentially complex system into a tool for wealth preservation. So as your financial situation evolves, consider professional guidance to figure out nuanced scenarios and to turn tax planning from a defensive necessity into an offensive advantage. With these steps in place, you’ll be equipped to keep more of what you earn, reduce unnecessary tax burdens, and build a more secure financial future Still holds up..